The Impact of the Additional Appropriations on Federal Spending in the Fourth District

Headlines regularly report large changes in federal spending. But despite recent additional appropriations, it appears that the federal funds flowing into the Fourth District in 2023 have returned to their prepandemic levels relative to the District’s gross domestic product.

The views authors express in District Data Briefs are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Harrison Markel.

Introduction

Over the last few years, there have been numerous headlines about large changes in federal spending. However, despite the recent additional appropriations, such as the infrastructure bill and the Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act, it appears that the federal funds flowing into the Fourth District in 2023 have returned to their prepandemic levels relative to the District’s gross domestic product (GDP).1 Social Security and federal medical outlays, which are driven more by retirements than by recent legislation, are now a higher share of the Fourth District’s GDP, but other federal spending has declined as a share of the District’s GDP for a few reasons. First, inflation increases nominal GDP, and federal programs that are not adjusted for inflation have not kept pace. Also, the massive appropriation figures that appeared in the headlines combine spending now with spending in the future and newly authorized spending with previously authorized spending that has now been repurposed. Examining the details of the legislation reveals much more modest spending increases this year. Federal outlays in the Fourth District are coming down from extreme highs that included pandemic relief programs, such as the American Rescue Plan Act (ARPA) funds. Although the end of pandemic relief transfers contributed to a return to normal of federal outlays in the Fourth District, state and local governments are still in the process of spending the ARPA funds they received in 2021 and 2022.

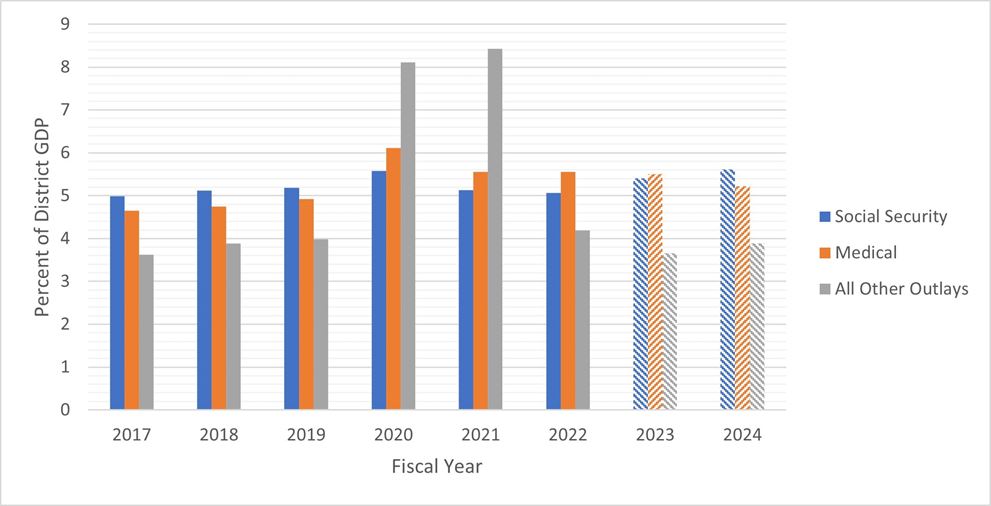

Overall trends in federal spending in the Fourth District

Figure 1 displays actual and estimated federal spending in the Fourth District as a percent of the District’s GDP.2 Outside the pandemic years of 2020 and 2021, Social Security and medical programs expend more money in the Fourth District than all other federal obligations combined. Increased federal spending in fiscal years 2023 and 2024 (FY23 and FY24) in the Fourth District will likely appear in Social Security and medical programs.3 The retirements of baby boomers are causing a long-term increase in Social Security and Medicare expenditures, and the pandemic pulled forward hundreds of thousands of those retirements (Montes, Smith, and Dajon, 2022). Social Security outlays in the Fourth District are estimated to rise from 5.2 percent of GDP in FY19 to 5.4 percent of GDP in FY23; medical spending is expected to rise from 4.9 percent of GDP to 5.5 percent. These correspond to $14.0 billion and $17.9 billion of additional outlays. In comparison, all other federal spending in the Fourth District is expected to have increased by $4.8 billion during the period. However, this increase does not keep pace with the growth of the District’s GDP. All other federal outlays in the Fourth District were equivalent to 4.0 percent of GDP in FY19, and they will be approximately 3.7 percent of GDP in FY23.

Figure 1. Federal Spending in the Fourth District

Notes: Textured bars indicate estimates. Obligations are reported by state and congressional district. The Fourth District totals include values for Ohio and the Pennsylvania, Kentucky, and West Virginia congressional districts that overlap the Fourth District.

Sources: US Department of the Treasury, Office of Management and Budget, Bureau of Economic Analysis, Congressional Budget Office, and author’s calculations.

The acts that changed federal appropriations

Three recent additional appropriations increased federal spending in FY23, FY24, and beyond: the Infrastructure Investment and Jobs Act (IIJA) in November 2021, the CHIPS and Science Act in August 2022, and the Inflation Reduction Act in August 2022. However, spending on many other federal programs did not grow as quickly as nominal GDP in the Fourth District. Recall from Figure 1, even with IIJA, CHIPS, and Inflation Reduction Act appropriations reflected in the “all other” values, the estimates are still below their prepandemic proportions of Fourth District GDP. The fourth major change to federal spending passed into law, the Fiscal Responsibility Act (FRA) in June 2023, will reduce spending growth for FY24, beginning in October.

Despite the IIJA’s enormous headline figure of $1.2 trillion, new spending in the Fourth District states this year will probably be only about $2.6 billion, or one-tenth of 1 percent of the District states’ GDP (Tomer et al., 2021).4 Table 1 summarizes the federal distributions to Fourth District states, those states’ awards through 2023:Q1, and the implied remaining funds. The vast majority of the IIJA funds have already been awarded by states in the Fourth District. Awarded funds will be paid out to contractors as work is completed. When we think about whether the IIJA funds are providing stimulus—that is, increasing spending and activity beyond that of a typical year—we might discount the stimulative effect of this spending by recognizing that about half of this infrastructure funding would have been available without the IIJA. Only $550 billion of the budget authorization was new; $650 billion of the spending is a continuation of the subsidies the federal government directs to infrastructure every year. The IIJA’s $1.2 trillion total is also a five-year sum. Using past experiences with the pace of infrastructure spending, the Congressional Budget Office anticipated that a small fraction of the outlays would occur in FY23, and the spending would increase each year over the next four years (Congressional Budget Office, 2022d).

Table 1. Infrastructure Investment and Jobs Act Funding and Awards in FY 2023

| Received ($B) | Awarded ($B) | Remaining ($B) | Remaining as a Percent of State GDP | |

|---|---|---|---|---|

| Ohio | 1.7 | 1.7 | 0.0 | 0.00% |

| Pennsylvania | 2.3 | 2.1 | 0.3 | 0.03% |

| Kentucky | 0.9 | 0.9 | 0.0 | 0.01% |

| West Virginia | 0.7 | 0.6 | 0.0 | 0.05% |

| All Other States | 47.2 | 44.1 | 3.1 | 0.01% |

Notes: State gross domestic product values are 2022 estimates. The received values are the total of road and bridge formula funding for FY23. The Association of Road and Transportation Builders of America has calculated the state-by-year allocations of IIJA road and bridge funding, which are the majority of the IIJA appropriations. Numbers may not add up due to rounding.

Sources: Association of Road and Transportation Builders of America, General Services Administration, Bureau of Economic Analysis, and author’s calculations.

The headline figure for the CHIPS and Science Act was $279 billion, but as with the IIJA, $200 billion of that spending was authorized in prior legislation and only refocused by the CHIPS and Science Act. Of the $79 billion of new expenses, approximately one-third will take the form of tax breaks for companies that expand domestic chip production (Congressional Budget Office, 2022a). The Congressional Budget Office predicted tax credit take-up would cost $3.0 billion in FY23 and $5.6 billion in FY24. The tax credits are already motivating corporate investment, with the Intel plant in our District being a high-profile example. Like the law’s tax expenditures, the CHIPS and Science Act’s direct expenditures are back loaded: $2.3 billion of additional direct expenditures are projected to occur in FY23, and $5.6 billion are projected to occur in FY24 (Congressional Budget Office, 2022b). The majority of the outlays the act authorizes are projected to happen in 2025 and beyond.

The Inflation Reduction Act is intended to be a fiscal contraction, meaning it increases taxes by more than it increases spending. Taxpayers’ spending should decrease by more than the government’s spending increases, and the total demand in the economy will be lower. Supply and demand set prices, so this reduction of total demand should reduce inflation. The Inflation Reduction Act generates additional federal revenue via increased corporate and individual taxes. The law also allows the federal government to negotiate with pharmaceutical companies for lower drug prices, which should reduce federal health expenditures. Inflation Reduction Act spending increases are mainly in clean energy investments and in extending Affordable Care Act subsidies. The Congressional Budget Office estimates that Inflation Reduction Act expenditures will be $27 billion in FY23 and $26 billion in FY24. The new spending will be offset by tax revenue increases of $44 billion in FY23 and $22 billion in FY24 (Congressional Budget Office, 2022c).

The most recent high-profile congressional action regarding spending was the reductions negotiated with the lifting of the debt ceiling. The headline from this legislation was a reduction of the deficits by a total of $1.5 trillion over the next 10 years (Shear, 2023). The Fiscal Responsibility Act of 2023 reduces discretionary budget authority in FY24 and beyond, but it will have only small effects on spending this year (Congressional Budget Office, 2023b). The negotiations avoided undoing most provisions of the IIJA and the Inflation Reduction Act. While some unspent pandemic relief funds were redirected to other line items, the law did not recall any of the unspent ARPA funds that are currently held by state and local governments (National Association of Counties, 2023). Social Security and most medical spending is considered mandatory, and the cuts focused on nondefense discretionary (that is, nonmandatory) spending. In FY24, among discretionary categories, defense spending will be allowed to grow up to 3 percent, and nondefense spending will be cut 9.7 percent below the FY23 levels.

The remaining American Rescue Plan Act funds

During the pandemic, there was great concern about how much state and local tax revenues would decline because of the lockdowns (Whitaker, 2020). Local government budget cuts could exacerbate regional economic slowdowns as they did during the Great Recession. In March 2021, Congress sought to prevent this when it authorized $1.9 trillion of additional spending in the ARPA (Stamm and Linke, 2021). The second largest portion of the expenditures, after the stimulus checks, was the $350 billion distributed to state, local, and tribal governments. Fortunately, the states and most major cities in the Fourth District are no longer relying on ARPA funds to replace lost revenue. Ohio, Kentucky, and West Virginia all passed FY23 budgets that reduce some tax rates and still anticipate sufficient revenues to balance expenditures or to have a surplus (Brainerd, 2023; Staver and Bischoff, 2023). Pennsylvania budgeted for 8 percent growth in revenues and expenditures (Shapiro, 2023). Among the Fourth District’s central cities, Cleveland, Columbus, Lexington, Dayton, and Toledo have all passed operating budgets that did not rely on ARPA funds to replace revenues (City of Dayton, 2023; Gagnet, 2023; Astolfi, 2023). Pittsburgh is still using ARPA funding because it built a portion of its ARPA allocation into each operating budget from FY21 to FY24 (City of Pittsburgh, 2022). Cincinnati and Akron reported using ARPA funds in FY23, covering 4.2 percent and 1.8 percent of their operating budgets, respectively (City of Cincinnati, 2023; Weldon, 2023; Becka, 2023).

Rather than being heavily used in operating budgets, the ARPA funds are currently flowing into local economies via a wide variety of grants and expenditures. Projects receiving funding include subsidies for affordable housing, construction of bike paths, upgrading of public health laboratories, and replacement of lead water lines. Beyond their usual spending in the next 18 months, the Fourth District’s state and local governments will be in the process of spending the approximately $12.9 billion of APRA funds they received from the federal government in FY21 and FY22 (see Table 2).5 The ARPA funds must be obligated through contracts or grant agreements by December 31, 2024, and paid out before the end of 2026. As detailed in Table 2, this could raise spending by the equivalent of 0.6 percent of the states’ GDP. According to the US Department of the Treasury, $27.5 billion was distributed to Fourth District states and local governments in those states. The National Conference of State Legislatures reported that Fourth District states have allocated $10.8 billion of their ARPA funds (National Conference of State Legislatures, 2023).6 The local governments in the Fourth District have awarded $3.7 billion of their $11.3 billion of ARPA funds according to data collected by Brookings Metro, the National Association of Counties, and the National League of Cities (2023) (Brachman and Haskins, 2023).7

Table 2. American Rescue Plan Allocations and Remaining Funds

State Government Allocation

| Received ($B) |

Allocated ($B) | Remaining ($B) | Remaining as a Percent of State GDP | |

|---|---|---|---|---|

| Ohio | 5.4 | 2.1 | 3.3 | 0.40% |

| Pennsylvania | 7.3 | 6.5 | 0.8 | 0.09% |

| Kentucky | 2.2 | 1.4 | 0.8 | 0.29% |

| West Virginia | 1.4 | 0.9 | 0.5 | 0.51% |

| Fourth District Total | 16.2 | 10.8 | 5.4 | 0.25% |

| All Other States | 179.1 | 141.2 | 37.9 | 0.16% |

Local Government Awards

| Received ($B) |

Awarded ($B) | Remaining ($B) | Remaining as a Percent of State GDP | |

|---|---|---|---|---|

| Ohio | 4.4 | 1.5 | 2.9 | 0.36% |

| Pennsylvania | 5.0 | 1.7 | 3.3 | 0.36% |

| Kentucky | 1.3 | 0.5 | 0.8 | 0.31% |

| West Virginia | 0.5 | 0.0 | 0.5 | 0.54% |

| Fourth District Total | 11.3 | 3.7 | 7.6 | 0.36% |

| All Other States | 98.3 | 45.0 | 53.3 | 0.23% |

Combined State and Local Government Totals

| Received ($B) |

Allocated ($B) | Remaining ($B) | Remaining as a Percent of State GDP | |

|---|---|---|---|---|

| Ohio | 9.8 | 3.6 | 6.3 | 0.76% |

| Pennsylvania | 12.3 | 8.3 | 4.1 | 0.44% |

| Kentucky | 3.4 | 1.9 | 1.6 | 0.61% |

| West Virginia | 1.9 | 0.9 | 1.0 | 1.05% |

| Fourth District Total | 27.5 | 14.5 | 12.9 | 0.61% |

| All Other States | 277.4 | 186.1 | 91.3 | 0.39% |

Notes: State gross domestic product values are estimates for 2022. Numbers may not add up due to rounding.

Sources: US Department of the Treasury, National Conference of State Legislatures, The Brookings Institution, Bureau of Economic Analysis, and author’s calculations.

In appendix Table A1, sums are displayed for only the ARPA-funded projects that are located in the Fourth District counties of Pennsylvania, Kentucky, and West Virginia.8 The local governments in the Fourth District counties have awarded a slightly higher proportion of their funds than all local governments in the Fourth District states: 36 percent ($2.3 billion of $6.4 billion) rather than 33 percent ($3.7 billion of $11.3 billion).

Conclusion

Although the large streams of federal pandemic relief dollars are no longer flowing into the Fourth District, spending remains elevated in some areas. Specifically, Social Security and medical transfers are likely to add the equivalent of eight-tenths of 1 percent of the Fourth District’s GDP beyond their 2019 levels. Also, state and local governments are still holding ARPA funds, and these will be spent in the near future. These ARPA funds represent another six-tenths of 1 percent of the Fourth District’s GDP. When considering how much stimulus might be provided by the recent additional appropriations, the headline numbers must be taken with a grain of salt. The multi-trillion-dollar totals conflate new authorizations with reauthorizations and spending this year with spending over the next decade. By focusing on funds that are likely to be spent in the Fourth District this year, we can anticipate that they will increase spending by approximately 1 percent of GDP beyond the levels from 2019, the last prepandemic year.9

Footnotes

- The Fourth District is the region that the Federal Reserve Bank of Cleveland serves. It contains all of Ohio, eastern Kentucky, western Pennsylvania, and the panhandle of West Virginia. Return to 1

- Historical data on obligations are from the US Department of the Treasury’s USAspending.gov. Fourth District GDP figures are aggregations of county GDP estimates from the Bureau of Economic Analysis. To estimate the Fourth District’s federal obligations in FY23 and FY24, FY22 obligations are increased by the growth for each type of spending displayed in the Office of Management and Budget’s Table 3.2. To estimate the Fourth District’s GDP in 2022, District counties’ GDP in each state is increased by the BEA’s estimate of state GDP growth. To estimate Fourth District GDP in 2023 and 2024, the District’s GDP estimate for 2022 is increased by the CBO’s estimate of national GDP growth for those years. Return to 2

- Federal budget and outlay values are reported for federal fiscal years. Fiscal years begin and end one quarter ahead of the calendar year. For example, FY23 began on October 1, 2022, and ends on September 30, 2023. Return to 3

- States in the Fourth District received $5.6 billion in IIJA funding, and approximately 46 percent of the IIJA funding is new funding rather than reauthorized funding; therefore, the “new” fund is approximately 0.46 x $5.6 B = $2.6 B. Return to 4

- While measures of ARPA fund outlays would be ideal, they are not available. Some measures of allocation and awards are available. “Allocation” refers to a legislative body budgeting funds for a specific purpose, which may specify the nongovernmental entity that will receive payment, or it may start a bidding process. “Award” refers to a later step during which a contract or agreement is signed, obligating the government to pay the specified entity or the winning bidder. Outlays would measure the final step when money has been transferred to the recipient or contractor. Return to 5

- The National Conference of State Legislatures data are intended to measure the uses of funds, so they record when funds are budgeted for a specific project. They do not measure obligations or outlays of the funds. Return to 6

- Local award data were last updated in December 2022. Return to 7

- Table 2 reports ARPA awards for all local governments in the Fourth District states so that the award totals can be added to the state allocations and scaled by the state GDP. Return to 8

- The contributions to this change mentioned above are Social Security (+0.2), medical (+0.6), all other outlays (-0.3), and ARPA funds (+0.6). Return to 9

References

- Astolfi, Courtney. 2023. “Cleveland City Council Passes 2023 Budget with a Few Changes from Mayor’s Plan.” Cleveland.com, March 20, 2023. https://www.cleveland.com/news/2023/03/cleveland-city-council-to-pass-2023-budget-with-a-few-changes-from-mayors-plan.html.

- Becka, Megan. 2023. “Akron City Council Approves 2023 Operating Budget; Highlights Include Raises for City Employees, Funds to Help Residents with Medical Debt.” Cleveland.com, March 29, 2023. https://www.cleveland.com/akron/2023/03/akron-city-council-approves-2023-operating-budget-highlights-include-raises-for-city-employees-funds-to-help-residents-with-medical-debt.html.

- Brachman, Lavea, and Glencora Haskins. 2023. “The American Rescue Plan, Two Years Later: Analyzing Local Governments’ Efforts at Equitable, Transformative Change.” Commentary. Brookings. March 9, 2023. https://www.brookings.edu/articles/the-american-rescue-plan-two-years-later-analyzing-local-governments-efforts-at-equitable-transformative-change/.

- Brainerd, Jackson. 2023. “2023 Mid-Year State Tax Actions Update.” Brief. National Conference of State Legislatures. https://www.ncsl.org/fiscal/2023-mid-year-state-tax-actions-update.

- Brookings Metro, National Association of Counties, and National League of Cities. 2023. “Local Government ARPA Investment Tracker.” Brookings. February 6, 2023. https://www.brookings.edu/articles/arpa-investment-tracker/.

- City of Cincinnati. 2023. “Fiscal Year 2023 Approved All Funds Budget Update.” Cincinnati, Ohio: City Manager’s Office, Office of Budget and Evaluation. https://www.cincinnati-oh.gov/sites/budget/assets/_City%20of%20Cincinnati%20Budget%20Book%20Update%20Approved%2003-06-2023%20FINAL%20FIXED%20with%20Cover.pdf.

- City of Dayton. 2023. “City Manager’s 2023 Recommended Budget.” City Commission Work Session. Dayton, Ohio. https://www.daytonohio.gov/DocumentCenter/View/13078/2023-Budget-Overview.

- City of Pittsburgh, Pittsburgh City Council. 2022. “2023 Operating Budget & Five Year Plan.” Pittsburgh, PA. https://pittsburghpa.gov/omb/budgets-reports.

- Congressional Budget Office. 2022a. “Legislation Enacted in the First Session of the 117th Congress That Affects Mandatory Spending or Revenues.” Report. https://www.cbo.gov/publication/57732.

- Congressional Budget Office. 2022b. “Table 2. Estimated Budgetary Effects of Divisions A and B of H.R. 4346, as Amended by the Senate and as Posted by the Senate Committee on Commerce, Science, & Transportation on July 20, 2022.” Cost Estimate. https://www.cbo.gov/publication/58319.

- Congressional Budget Office. 2022c. “Estimated Budgetary Effects of H.R. 4346, as Amended by the Senate and as Posted by the Senate Committee on Commerce, Science, and Transportation on July 20, 2022.” Cost Estimate. https://www.cbo.gov/publication/58319.

- Congressional Budget Office. 2022d. “Estimated Budgetary Effects of H.R. 5376, the Inflation Reduction Act of 2022, as Amended in the Nature of a Substitute (ERN22335) and Posted on the Website of the Senate Majority Leader on July 27, 2022.” Cost Estimate. https://www.cbo.gov/system/files/2022-08/hr5376_IR_Act_8-3-22.pdf.

- Congressional Budget Office. 2023a. “The Budget and Economic Outlook: 2023 to 2033.” Report. https://www.cbo.gov/publication/58848.

- Congressional Budget Office. 2023b. “CBO’s Estimate of the Budgetary Effects of H.R. 3746, the Fiscal Responsibility Act of 2023, As Posted on the Website of the House Committee on Rules on May 28, 2023.” Cost Estimate. https://www.cbo.gov/publication/59225.

- Gagnet, Nancy. 2023. “Toledo City Council Approves $996M Operating Budget.” Toledo Blade, February 21, 2023. https://www.toledoblade.com/local/city/2023/02/21/toledo-city-council-approves-996m-operating-budget/stories/20230221127.

- Montes, Joshua, Christopher L. Smith, and Juliana Dajon. 2022. “‘The Great Retirement Boom’: The Pandemic-Era Surge in Retirements and Implications for Future Labor Force Participation.” Working Paper 2022-081. Finance and Economics Discussion Series. Washington: Board of Governors of the Federal Reserve System. https://doi.org/10.17016/FEDS.2022.081.

- National Association of Counties. 2023. “Legislative Analysis for Counties: The Fiscal Responsibility Act of 2023.” https://www.naco.org/resources/legislative-analysis-counties-fiscal-responsibility-act-2023.

- National Conference of State Legislatures. 2023. “ARPA State Fiscal Recovery Fund Allocations Database.” Accessed July 28, 2023. https://www.ncsl.org/fiscal/arpa-state-fiscal-recovery-fund-allocations.

- Shapiro, Governor Josh. 2023. “Budget in Brief 2023-2024.” Harrisburg, PA: Office of the Governor, Commonwealth of Pennsylvania. https://www.budget.pa.gov/Publications%20and%20Reports/CommonwealthBudget/Documents/2023-24%20Budget%20Documents/Budget%20in%20Brief%202023-24%20Web.pdf.

- Shear, Michael D. 2023. “Biden Signs Fiscal Responsibility Act in End to Debt Limit Crisis.” The New York Times, June 3, 2023, sec. Politics. https://www.nytimes.com/2023/06/03/us/politics/biden-debt-bill.html.

- Stamm, Stephanie, and Maureen Linke. 2021. “What Is in the Third Covid-19 Stimulus Package?” The Wall Street Journal, March 11, 2021, sec. Politics. https://www.wsj.com/articles/whats-new-in-the-third-covid-19-stimulus-bill-11615285802.

- Staver, Anna, and Laura A. Bischoff. 2023. “Income and Sales Tax Cuts Part of Massive Ohio Budget Passed by House.” The Columbus Dispatch, April 26, 2023, sec. Politics. https://www.dispatch.com/story/news/politics/2023/04/26/ohio-house-to-vote-on-budget-with-more-money-for-medicaid-schools/70150455007/.

- Tomer, Adie, Caroline George, Joseph W. Kane, and Andrew Bourne. 2021. “America Has an Infrastructure Bill. What Happens Next?” Commentary. Brookings. November 9, 2021. https://www.brookings.edu/articles/america-has-an-infrastructure-bill-what-happens-next/.

- US Bureau of Economic Analysis. 2022. “Gross Domestic Product by County, 2021.” GDP by County, Metro, and Other Areas. December 8, 2022. https://www.bea.gov/data/gdp/gdp-county-metro-and-other-areas.

- US Bureau of Economic Analysis. 2023. “Gross Domestic Product by State and Personal Income by State, 1st Quarter 2023.” GDP by State. June 30, 2023. https://www.bea.gov/data/gdp/gdp-state.

- US Department of the Treasury. n.d. “Coronavirus State and Local Fiscal Recovery Funds.” US Department of the Treasury: Policy Issues. Accessed July 24, 2023. https://home.treasury.gov/policy-issues/coronavirus/assistance-for-state-local-and-tribal-governments/state-and-local-fiscal-recovery-funds.

- USAspending. n.d. “Federal Awards Advanced Search.” USAspending.Gov. Accessed July 24, 2023. https://usaspending.gov/search.

- Weldon, Casey. 2023. “Cincinnati’s Budget Draft Looks to Address City Services, Long-Term Concerns.” Spectrum News 1, May 26, 2023, sec. Politics. https://spectrumnews1.com/oh/columbus/news/2023/05/26/city-budget-proposal-looks-to-address-long-term-revenue-concerns.

- Whitaker, Stephan D. 2020. “How Much Help Do State and Local Governments Need? Updated Estimates of Revenue Losses from Pandemic Mitigation.” Cleveland Fed District Data Briefs. Federal Reserve Bank of Cleveland. https://doi.org/10.26509/frbc-ddb-20200629.

Appendix

Local governments in Fourth District counties have awarded 36 percent of their ARPA funds.

Table A1. American Rescue Plan Act Local Allocations and Awards for Local Governments in Fourth District Counties

Local Government Allocations

| Received ($B) | Allocated ($B) | Remaining ($B) | Remaining as a Percent of the State's Fourth District GDP | |

|---|---|---|---|---|

| Ohio | 4.4 | 1.5 | 2.9 | 0.36% |

| Pennsylvania | 1.4 | 0.7 | 0.7 | 0.31% |

| Kentucky | 0.5 | 0.1 | 0.4 | 0.36% |

| West Virginia | 0.1 | 0.0 | 0.1 | 0.48% |

| Fourth District Total | 6.4 | 2.3 | 4.1 | 0.35% |

| All Other Local Governments | 103.1 | 46.4 | 56.8 | 0.23% |

Note: State GDP values are estimates for 2022.

Sources: US Department of the Treasury, The Brookings Institution, Bureau of Economic Analysis, and author’s calculations.

Suggested Citation

Whitaker, Stephan D. 2023. “The Impact of the Additional Appropriations on Federal Spending in the Fourth District.” Federal Reserve Bank of Cleveland, Cleveland Fed District Data Brief. https://doi.org/10.26509/frbc-ddb-20230829

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International

- Share